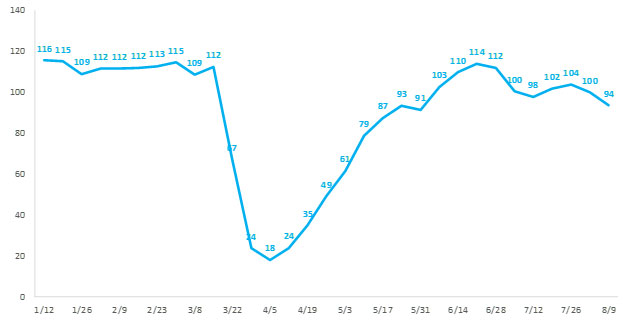

Used Market Update: August 13, 2020

Wholesale auction sales of vehicles up to 8 years old for the week ending August 9 declined 6% vs. the previous week (week ending August 2) with sales again reaching an estimated 94,000. While sale volumes remain healthy, sales over the past two weeks have been approximately 5% less than the JD Power pre-virus forecast for each respective period.

Weekly Wholesale Auction Sales (thousands)

Segment-level auction sales on the mainstream side of the market were reduced an average of 6%. Small car sales declined the most, down an average of 13% for the week. Following closely behind, large pickup and compact SUV sales each declined 10%. Midsize SUV sales increased a slight 1%, however, remaining mainstream segments experienced sales declines for the period. Premium segment sales increased by a collective average of 3% for the week, however, results were mixed once again. For example, compact and small premium SUV sales rose 18% and 19%, respectively. While, on the opposite end of the spectrum, large premium car sales declined 17%.

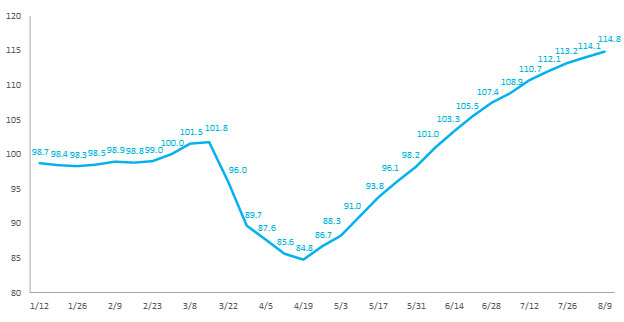

Wholesale Auction Prices Increase, Rate of Growth Slows

Wholesale auction prices improved for the 16th consecutive week, rising 0.8 percentage points for the week. The rate of growth continues to slow as last week’s result was the fourth consecutive week of slowing price appreciation and the smallest week-over-week increase recorded since prices began their recovery in April. However, prices have grown 35% over the past 16 weeks and are now 15% higher than at the beginning of March.

Weekly Wholesale Auction Price Index (Mar 1 = 100)

Wholesale prices for mainstream segments the week ending August 9 increased an average of 0.7% vs. the prior week. Large pickup prices were the strongest, increasing an average of 1.3%, followed closely by small car prices that grew 1%. Remaining mainstream segments each experienced positive price movement for the period. Premium prices once again performed slightly better than their mainstream counterparts. On average, premium segment prices increased 0.9%, which was driven by small and large car increases of 2.1% each. Premium SUV results were mixed, midsize and compact premium SUV prices rose 0.7% and 1.1%, respectively. Small premium SUV prices were flat and large premium SUV prices fell a slight 0.2%.

While wholesale prices remain strong, the declining rate of growth week over week indicates a slowing market. Prices are expected to level off in August as pent-up demand wanes and pandemic-related macro-economic headwinds increase. By year's end, prices are expected to be on par with pre-virus levels. It is important to note, however, that while the outlook is relatively optimistic, there remains a great deal of uncertainty surrounding the effect of new virus outbreaks, the potential for another round of federal stimulus, and overall employment conditions. Given these unknowns, a heightened degree of market volatility should be expected.

Used Vehicle Retail Sales Performance Dropped While Prices Continued to Rise

Sales of used vehicles at franchised dealers were 1% above pre-virus forecast for the week ending August 9. The result reflected a 2% decline week over week vs. forecast. However, used retail prices continued to rise, increasing 1.7% for the week ending August 9. Prices are now 6.6% higher than the index baseline level from March 1.