Used Market Update: October 30, 2020

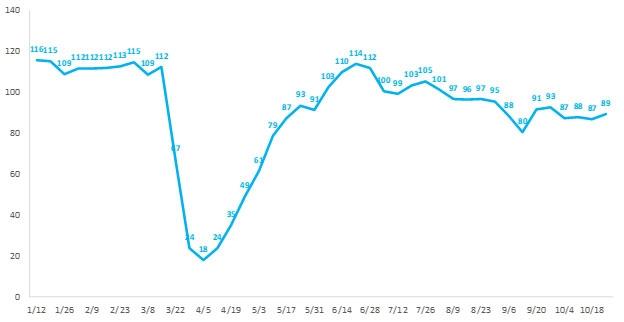

Wholesale auction sales of vehicles up to 8 years old for the week ending Oct. 25 improved reaching approximately 89,000 units. Last week’s result marks a slight increase after three weeks of relatively flat sales. Ultimately, sales for the week ending Oct. 25 were approximately 12% lower than what’s typically recorded for the period. Segment-level auction sales on the mainstream side of the market were mixed. Across segments, the general trend for the week were increases in passenger car sales and decreases in SUV sales. On the premium side of the market, sales were virtually down across the board, the only premium segment that experienced flat week-over-week sales was small premium car.

Weekly Wholesale Auction Sales (thousands)

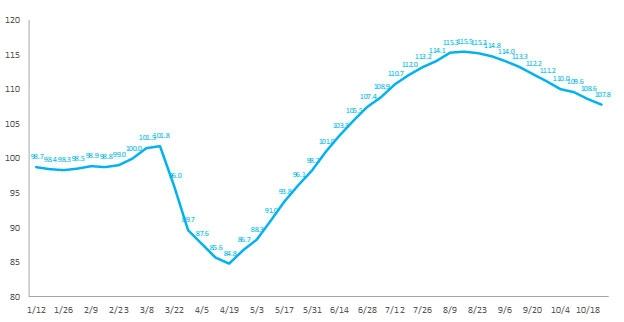

Wholesale Auction Prices Down Once Again

After several weeks of small price declines, wholesale auction prices moved lower again the week ending Oct. 25, marking the 10th consecutive week of downward price movement. Prices last week were reduced an average of 0.7%. As wholesale prices continue to soften, they remain 27% higher than their trough in April, and 8% above their level at the beginning of March.

Weekly Wholesale Auction Price Index (Mar 1 = 100)

Wholesale prices for mainstream segments declined by an average of 0.4% for the week ending Oct. 25 when compared with the prior week. Prices on the mainstream side were generally down, though large car prices increased 0.8% and midsize pickup prices increased 0.7%. Results for all other mainstream segments were flat or down, as prices fell between 0.4% (large SUV) and 1.7% (compact car). Premium prices performed in line with their mainstream counterparts. On average, premium segment prices fell 0.4%. Premium results were generally negative, however, large premium car prices increased 0.2%. Remaining premium segment prices feel between 0.3% (large premium SUV) and 0.8% (midsize premium car).

Despite a slowing used market, wholesale prices remain strong. Prices are expected to continue to move lower through November and December as pent-up demand has been satisfied and pandemic-related macro-economic headwinds increase. By year's end, prices are expected to be greater than pre-virus levels. It is important to note, however, that while the outlook is relatively optimistic, there remains a great deal of uncertainty surrounding the effect of new virus outbreaks, the potential for another round of federal stimulus and overall employment conditions. Given these unknowns, a heightened degree of market volatility should be expected.